Is the Gold Price Suppressed on the COMEX Futures Exchange?

From examining the roll data of gold futures contracts on the COMEX I have found no evidence of gold price suppression.

One of the most discussed topics in the gold space is long-term gold price suppression on the COMEX futures exchange in New York. It’s an interesting theory, because we know that in the past the United States has been active in “stabilizing” the gold price to make to dollar look stronger. But that was done openly in the 1960s and 1970s by selling physical gold. Is any entity still suppressing the gold price, and does it use the futures market?

Price manipulation through spoofing, which can be small intraday price movements up or down, has been proven time and again, but not long-term suppression.

Introduction

In a recent video precious metals commentator Andrew Maguire was talking about gold price suppression and mentioned that traders can roll large futures positions. Towards the regulator he stated:

What? You mean you can roll it over for ad infinitum? … If there is one thing you should focus on it is that.

Gold futures can indeed be rolled ad infinitum, just like corn, sugar, oil, stock indices, bond, FX, and crypto futures. Rolling is an essential feature of the futures market. Though, Maguire brings up an excellent point for investigating if a massive short position in the gold futures market is suppressing the price: the roll data.

How it Works

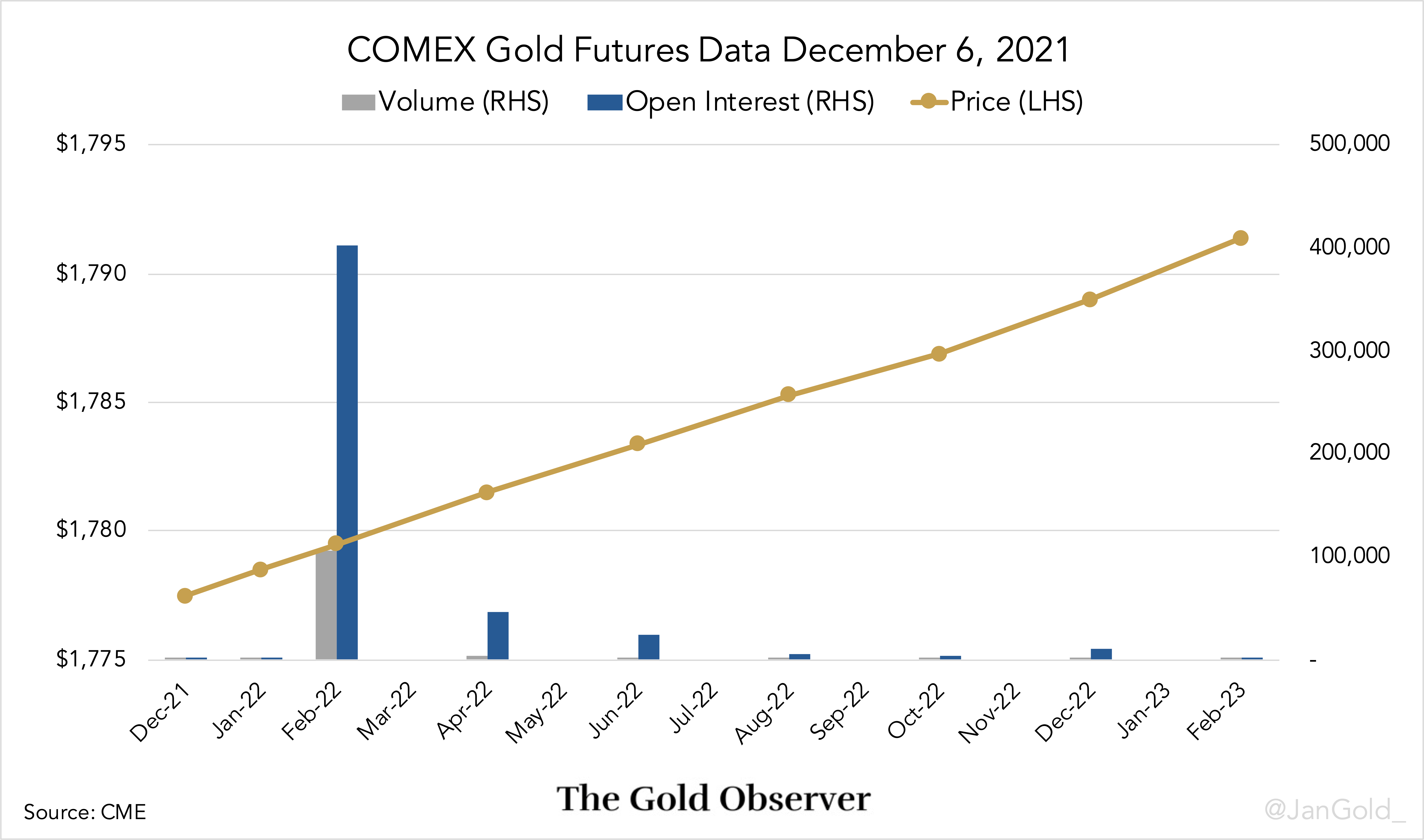

Futures can be traded many months into the future. For gold February, April, June, August, October and December are actively traded months—the rest be can ignored. The “near month” always captures the bulk of trading volume and open interest. At the time of writing the most actively traded contract (near month) on the COMEX is February.

Let’s run though a scenario of long-term price suppression on the COMEX, to subsequently examine roll data and see if this is actually happening.

Suppose, a crooked entity sells short hundreds of thousands of contracts. This is very difficult because the regulator sets position limits for all traders, but we will assume the crooked entity has found a way to circumvent the restrictions. The massive short is opened in the near month, driving down the futures price, and through arbitragers the futures price is translated to the spot market: the price of physical gold is suppressed too.

Now what? Any futures position will eventually expire. The massive short seller has three options. The first possibility is to close the short position by opening an opposite position. In case of a massive short position an equal amount of contracts will have to be bought long for the clearinghouse to net it all out. The result would be that the initial price suppression of the massive short would be undone—closing a short leads to the price going up. The second possibility for the massive short is to physically delivery the metal. From COMEX delivery data, however, we know only a small percentage of the open interest is physically delivered. No big short is delivering hundreds to thousands of tonnes of gold every other month.

The third possibility for the massive short is to roll, by closing its near month position and open a new massive short in the next active month. But a large roll would leave traces in futures prices. When a massive short is rolled the price of the expiring month is pushed up, and the price of the next active month is pushed down. The spread between the contracts—calculated as the next active month minus the near month—would decline during the roll period.

What I did is grab the settlement prices from the COMEX website and made a chart. Below you can see the progression of the spread (between the December 2021 and February 2022 contract) from the beginning of October until the end of November. The last day of November was the start of the delivery procedure for December, so most traders rolled (or closed) their December positions prior to that.

Clearly, the spread increased leading up to the end of November, signaling the longs were more eager to roll than the shorts. In other words, it looks like more longs than shorts rolled.

Conclusion

If there was any period suited for holding down the price of gold it was in the past few months when the world was shocked by the highest inflation numbers in 30 years. In the data at my disposal, however, I see no evidence of a massive short suppressing the gold price on the COMEX.

The only critique of my methodology I can think of is that I used settlement prices instead of bid and ask quotes. Unfortunately, I don’t have the resources to obtain the latter. Supporting my findings is a similar investigation performed by Keith Weiner from Monetary Metals (read here), who used spot and futures bid and ask quotes over several decades. His conclusion is the same as mine: there is no evidence for gold price suppression on the COMEX.

Having said that, I would be happy to change my mind if anyone has new evidence.

If you enjoyed reading this article please consider to support The Gold Observer and subscribe to the newsletter.

Finally some sense Jan, a good explantaion.

A lot of the 'noise' from those that think gold is suppressed is that they do not understand why the bullion banks have short futures positions.

Gold leasing books are now (mostly) funded by balance sheet (cash) as central bank lending reduced significantly in recent years as the yield crashed so the risk/reward was no longer there.

To fund gold leasing where the bullion banks lend metal to customers, which add up to significant volumes, they buy OTC gold (loco London for instance) and cover this position by selling futures. The banks are square, they have no significant short (or long for that matter) as is constantly claimed by some. As this short position reaches expiry they need to roll it as they remain long the OTC for the leasing book. Clean and simple.

This was evidenced last year when the pandemic lockdowns initially hit the EFP market where the difference between the London OTC market and the COMEX futures widened to levels never thought imaginable. This was because whilst the banks were long the London effectively, they were short the COMEX, and the global stoppage in transportation put those shorts in position whereby, even if they wanted to, they could not deliver metal to New York. Market participants knew this and offers dried up faster than a puddle in the Sahara. Mark to Market 'losses' on the books for some bullion banks that first week as a result were quite daunting with some closing them out. Others knew this would be temporary and held on to see this 'loss' evaporate. The less educated in the market initially claimed this was a flight to quality (of the COMEX gold) but failed to understand that it was a lack of liquidity that caused this as those that could offer knew they could just sit back potentially and cash in as those that capitulated realized their losses.

The problem we have is that there are too many experts, and that is a loose use of that term, that seem to only see the COMEX gold contract as the price of gold alone, and not understand the whole eco-system of gold. The price of gold is interlinked between the Comex, the OTC market and all the other places like the Indian physical market, the Shanghai gold exchange and central banks activity for it to be manipulated by just one of the cogs in that wheel.

Tin-foil hats off, reality googles on for some I think.

I would be most grateful if you could answer GATA's points below:

That is, the data does not show whether governments and central banks are selling gold contracts through brokers on the exchange.

If governments and central banks are selling gold futures, then gold price suppression is indeed government policy -- and there is much evidence that they are. For example:

1) At a hearing in U.S. District Court in Boston in November 2001 on GATA consultant Reg Howe's gold price manipulation lawsuit against the U.S. Treasury Department, Federal Reserve, Bank for International Settlements, and bullion banks that trade gold on the Comex, an assistant U.S. attorney declared that the U.S. government has the authority, under the Gold Reserve Act of 1934 and related statutes, to act on the gold price exactly as Howe's lawsuit complained:

https://www.gata.org/node/4211

2) Through its Central Bank Incentive Program, the operator of the New York Commodities Exchange, CME Group, gives governments and central banks special volume discounts for trading all futures contracts sold on the exchange, including gold contracts:

https://www.gata.org/node/18925

Such trading must be conducted through brokers approved by the exchange, which would provide camouflage for official interventions.

Would CME Group offer the discount program if it was never being used by governments and central banks?

3) The U.S. Commodity Futures Trading Commission, which regulates the New York Commodities Exchange, repeatedly has refused to say, even for a member of Congress, whether the commission has jurisdiction over manipulative futures trading undertaken by or at the behest of the U.S. government:

https://www.gata.org/node/20089

The commission's refusal to answer such a simple question about its jurisdiction is effectively confirmation that the U.S. government indeed is meddling in the gold futures market to defend the dollar and U.S. interest rates.

Analysis of futures market trading data doesn't tell much unless you also know the identities of the parties behind that trading. If governments and central banks are doing a big part of the selling in gold futures via intermediary brokers, the trading data alone won't reveal it. So Nieuwenhuijs' analysis here really doesn't address the price suppression issue. He's looking in the wrong place.